Tags

Banking Co-partnership Act 1826, Commercial Distress, Financial crisis 1825, Thomas Wilson, William Henry Baldock

The collapse of many banks was inevitable in a fragile and unregulated financial world. The country was still coming to terms with massive debts from successive wars that needed repaying. Combine this with bleak financial prospects, high unemployment, a disastrous famine and it was inevitable that businesses and trades would collapse.

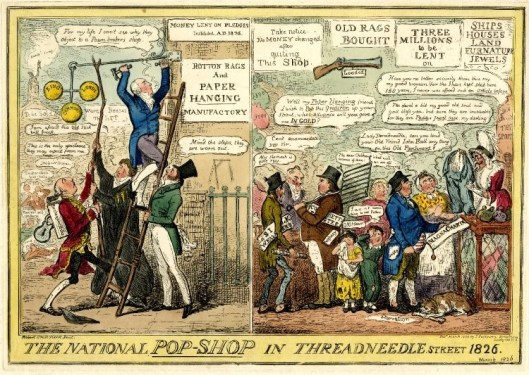

The financial crisis of 1825, in which the country claimed to have been “within twenty-four hours of barter” saw 93 banks in England and Wales fail (approximately 15 per cent) and resulted in widespread commercial distress.

The Banking Co-partnership Act, passed in 1826, was an attempt to stabilise the system. It changed the structure of banking in England and Wales by permitting the establishment of joint-stock banks (JSBs) outside a 65-mile radius of London. One hundred and thirty eight JSBs were created before the legislation was repealed in 1844.

The vulnerability and subsequent collapse of joint-stock banks was the major cause behind William Henry Baldock losses and bankruptcy. (There were other reasons why Baldock’s wealth deteriorated. The income and involvement in the free trade was fading into the background of history as smuggling became less profitable and worthy of risk. As Britain returned to peace after wars with America and France, the revenues from the Canterbury barracks fell significantly.) The Baldocks also found themselves living in an increasingly polarized world where new industries were taking over from traditional agriculture as the economic drivers. Investment in the new technologies brought about many financial failures as well as some successes.

The situation in 1826 threatened all classes. Simply put, it was exciting but shaking the very foundations of British life.

In Parliamentary procedures of February 1826, Thomas Wilson brought before Parliament, the current distress of business. Wilson was an established, prominent and prosperous London merchant. His firm of Wilson and Blanshard (previously Wilson, Agassiz and Company) operated from Jeffery’s Square. He had at one time been in Grenada, had an interest in the Atlantic trade and was a long-serving chairman of the Society of Merchants trading to the continent.

Thomas Wilson was ‘loudly called on by the House’ to address the situation on behalf of commercial enterprises. Before Parliament was the motion to establish a select committee which would ‘enquire into the present distresses of the commercial world.’

Before Wilson spoke, the Lord Chancellor told the House that a communication had taken place between his majesty’s Government and the Bank. The purpose was to establish how far that body would be disposed to extend relief to the existing depression in the trading, commercial, and manufacturing interests of the country.

The communiqué had been prompted by a debate in the House of Commons concerning a petition on behalf of London traders. In that debate, Thomas Wilson stated that he had never experienced greater anxiety in petitioning the house on the vital importance to the welfare of the country. The merchants of London had solicited his majesty’s government for relief, by an issue of Exchequer bills but the government had made up their minds to grant no relief.

The government presented several objections. Crucially, during the discussions it was discovered that the charter of the Bank of England enabled that body to lend money on goods. The government concluded that any interference on their part would be highly improper. Having established that the Bank was open to the relief of the mercantile classes the question arose of why the merchants did not apply to that body? What necessity was there for an issue of Exchequer bills under these circumstances? Thomas Wilson replied that it was a question of integrity and avoiding public embarrassment. A merchant who wanted an advance, not on imaginary security, but on real goods of value, could discreetly apply to the commissioners and overcome his difficulties without the circumstance of his temporary embarrassment being exposed.

The causes of the crisis that brought about so much commercial distress were complex. (See note below.) Contemporaries blamed country bankers and called for an overhaul of the banking system. The consequential legislation of 1826 – the 1826 Banking Co-Partnership Act – allowed for the establishment of banks with more than six partners and freely transferable shares outside a sixty-five mile radius of London. Thus ended the Bank of England’s monopoly of joint stock banking. It was an opportunity that William Henry Baldock couldn’t resist but one that he would bitterly regret as his wealth was eaten up by the collapse of the Canterbury Union Bank.

Notes:

Focus 1: “The crash of 1825-1826 was the first modern financial crisis. Unlike earlier speculative bubbles, the 1825 crisis was not caused only by exogenous circumstances like war or overzealous investment. The real cause of the 1825 crisis was the diversification of the finance economy into tiny investment units—a loan here, an insurance policy there—offered as seemingly responsible ways to maintain credit and generate capital. When the market finally did crash, no single group or class could be blamed for causing it. Economists came to realize that the market was always at the mercy of booms and busts and that no single individuals or professions within it could be said to be in charge of it. In other words, 1825 marks the moment at which capitalism grew from an ideological enterprise into a global condition. 1825 also marks a crucial transition in the publishing industry, the point at which the traditional market for vellum-bound epics and triple-decker novels was eclipsed by cheap reprints and serial publications. It thus signals the end of what we might call the Romantic ideal and the emergence of an existential malaise in English literature that persists in Victorian writing and beyond.” Alexander J. Dick.

Focus 2: The story has resonance for three reasons: (1) The crisis was probably the first example of an emerging market induced financial crisis. (2) It offers an early lesson on the importance of timely lender-of-last-resort intervention by the monetary authorities. (3) It provides valuable insights on the role of information in credit markets, as Larry Neal emphasizes in his paper. Michael D. Bordo

References:

Because of its important lessons, issues and topicality for modern finance and corporate governance, there is a huge library regarding the financial crisis during 1825-26. Below are a few references with an emphasis on what happened and subsequent implications:

Commercial Distress. House of Commons Debate 28 February 1826

Change and continuity: the development of joint stock banking in the early 19th century Lucy Newton, Centre for International Business History, University of Reading

The Financial Crisis of 1825 and the Restructuring of the British Financial System. Larry Neal

On the Financial Crisis, 1825 – 26 Alexander J. Dick

Pingback: A nation panics. Closure of the banks and the 1825 aftershock. | Blue Anchor Corner

Pingback: All Things History – Monthly Roundup – All Things Georgian